Our latest research strongly suggests that a highly dynamic market access situation in the US is feeding back into upstream decisions around R&D strategy. We explored this topic in detail in a recent white paper called Working Backwards: Patient access strategy is now guiding R&D.

This article briefly summarizes the first half of the report. From compressed drug lifecycles through to therapeutic area priorities, drug developers are resetting as the status quo shifts. Policymakers are looking to wield greater control over drug pricing, while payers and providers are becoming more creative in shifting the cost burden of new medicines. And so what may have previously been the correct strategy is coming under review.

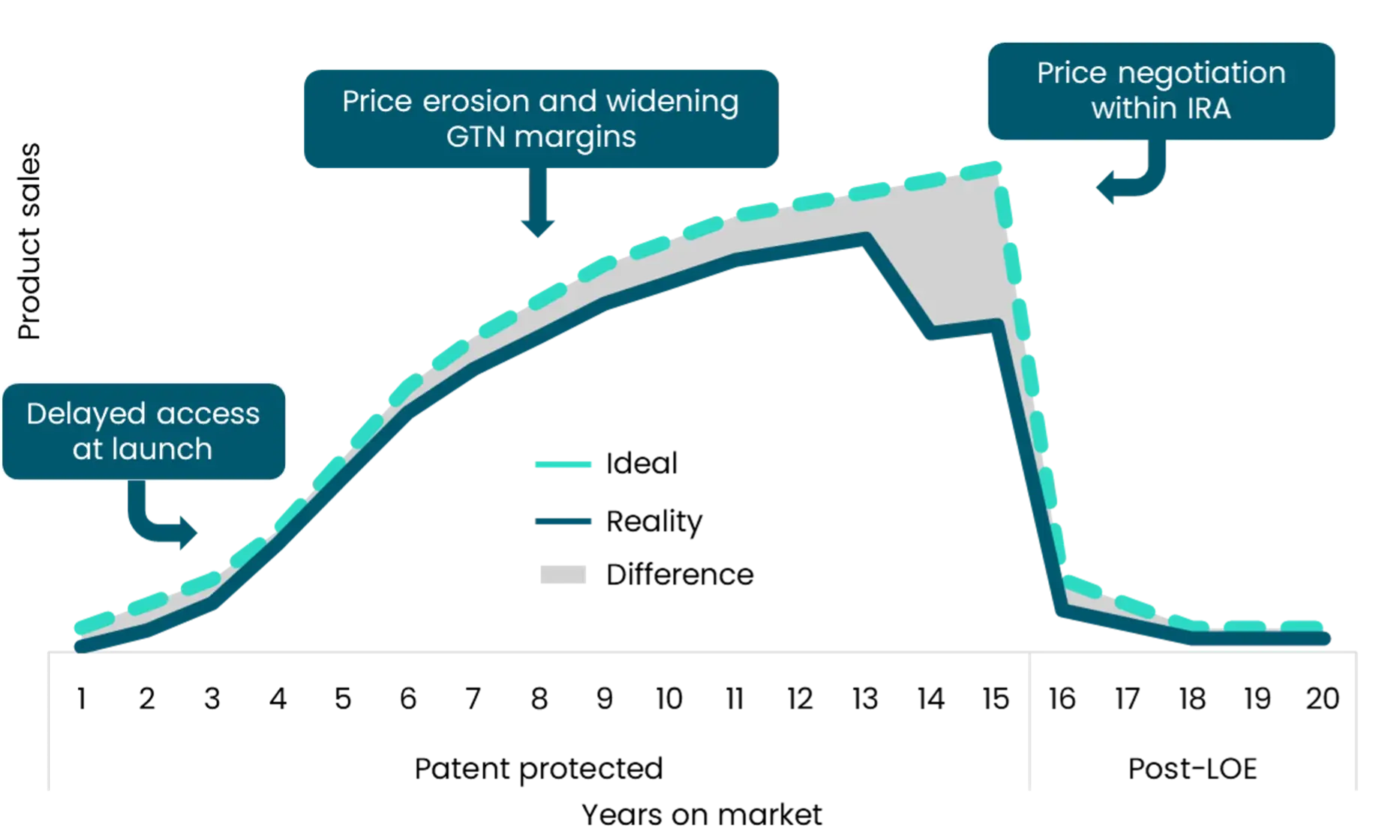

Compression

Pharma companies are facing multiple challenges in their pursuit of launching novel drugs and maximizing value throughout their lifecycle. MMIT research shows that new-to-market blocks and delayed coverage decisions are contributing to slow uptake of new therapies. This is partly a consequence of the increasing use of accelerated regulatory pathways and the complexity of modern medicine. Although payers are also becoming more active in managing costs and limiting exposure to expensive new therapies.

Beyond the crucial launch stage – which can often determine the overall trajectory of a drug – pharma companies continue to feel the squeeze. The Inflation Reduction Act (IRA) continues to shape drug lifecycles, and not just after 13 years during which price negotiation can come into play. The inflation rebate component of the act also curbs annual price increases, which have supported many products’ growth. And with new proposals such as most-favored nation pricing (MFN), pharma has less ability to set higher prices at launch to compensate. Even before MFN is codified, pharma is changing its global approach to pricing and exploring new direct-to-patient business models.

These new influences aside, pressures from expansion of the 340B program and the rise of group purchasing organization (GPO) contracts further widen the gross-to-net margin. The visual below summarizes these factors for a hypothetical new drug launch.

Illustrative lifecycle compression

Source: Norstella

R&D prioritization

It is perhaps inevitable that these downstream challenges are influencing decisions far upstream concerning R&D strategy and prioritization. Pharma companies are now increasingly valuing drugs with the potential for a fast launch, targeted at areas of reduced competition, and with greater control over pricing. This is evident in the shift within drug pipelines.

An analysis of Citeline’s Pharmaprojects database shows that certain therapeutic groups are gaining in prominence at the expense of others. While the overall pipeline itself continues to increase – last year’s figure was 4.6% – large numbers of candidates were terminated to make way for new programs. And within this churn, we can see the shift in pharma’s R&D priorities.

Oncology continues to top the list for new drug discovery, but this year marks the first time in well over a decade that oncology grew at a below-average rate. Competitive intensity – at both the R&D and patient access stages – saw oncology’s relative share of the pipeline peak at 40%. With such a large share of recent drug approvals, and a significant Medicare population, the tide has finally turned.

Rather, rare diseases and cardiovascular diseases both saw notable above-average increases in drug development. The rare disease space in particular is more receptive to creative patient access solutions and less exposed to the IRA. The renaissance in cardiovascular diseases coincides with a greater focus on improved long-term outcomes associated with anti-obesity medicines, particularly as these treatments shift into younger and overall healthier patients.

Pipeline churn during 2024

Source: Citeline